Mexico. The year 2019 was characterized for the telecommunications sector, as one permeated by macroeconomic and national political uncertainty, coupled with trade tensions and geopolitical conflicts. All this resulted internationally in increasing transaction costs in the flow of exchange of goods and services, which consequently reduced the economic growth of the countries. There, Mexico has been no exception.

Mexico. The year 2019 was characterized for the telecommunications sector, as one permeated by macroeconomic and national political uncertainty, coupled with trade tensions and geopolitical conflicts. All this resulted internationally in increasing transaction costs in the flow of exchange of goods and services, which consequently reduced the economic growth of the countries. There, Mexico has been no exception.

In this scenario, the International Monetary Fund (IMF) forecasts global growth of just 3.0%, its lowest level since 2008–2009, with a slight rebound to 3.4% in 2020.

In line with the world, the national economy has been experiencing for several months a scenario of stagnation, in the best of cases, resulting from the limited dynamism of investment and private consumption, again, resulting from the uncertainty in economic policies, the weakening of global manufacturing activity and the rising costs of indebtedness, among many other factors.

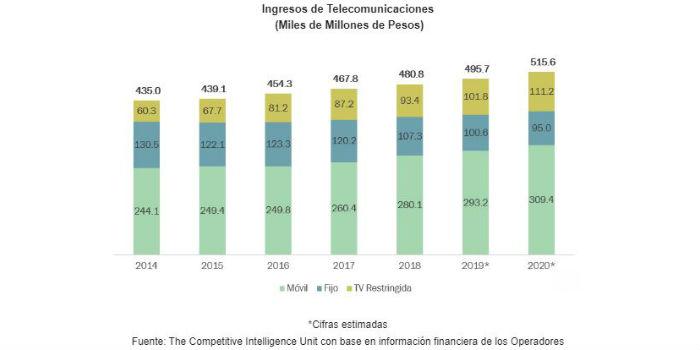

Telecommunications Revenues in 2019

Despite the fact that economic forecasts show a slowdown/stagnation in growth and even a contraction in real terms, the telecommunications sector is seeing an upward trend in revenues.

The telecommunications sector has not been absent from these macro effects, but it still retains positive growth rates. Thus, the provision of voice and data services, coupled with the sale of mobile equipment in Mexico, will generate revenues of $495.7 billion pesos, 3.1% more than in 2018.

The factors that explain this dynamic include the growing contracting of Pay-TV services, the internet and the different packaging of services, as well as the growing consumption of mobile services, mainly data. This is accompanied by the sustained growth in the sale of smart devices by operators in the mobile segment, sales that unbalance the national equipment of smartphones towards the medium and high ranges in two thirds of the total of 106 million that already operate in the country.

Dynamics of Market Segments

In its dynamics by segment, two of the three segments that make up the sector report positive and significant growth in 2019.

On the one hand, restricted television and packaging continue to register an accelerated pace of growth that drives the sectoral aggregate, representing the second component by its weighting (20.5%) on total revenues, after the mobile segment (59.2%). Growth of 9.0% is anticipated at the end of 2019, close to the double-digit range that characterized it in previous years. For 2020, it is anticipated to continue at a similar pace of revenue growth.

This segment also stands out for better conditions in the provision of services, for example, in terms of price, download speed, greater number of TV channels and / or inclusion of video on demand platforms over the internet.

For its part, mobile telecommunications will register a slowdown in their dynamics compared to 2018, a growth of 4.7% is expected for 2019, that is, 2.9 percentage points (p.p.) less than a year ago. Although there is an increase in the average consumption of mobile services per user, especially that of mobile data or megabytes of Internet browsing, the slowdown in the sale of smartphones or smartphones explains the lower growth of the segment.

With regard to fixed telecommunications (20.2% of total sectoral revenues), although there is a sustained increase in the contracting of fixed internet in homes and companies in the country, the fixed segment as a whole (voice and data) will close the year with an even more pronounced contraction than in previous ones, with a rate of -6.2% in terms of income. This derives from the continued categorical replacement of fixed telephony as a means of communication for Mexican households.

Forecasts for 2020

It is reasonable to anticipate that this revenue trajectory by segment will result in a path of positive growth of the sector as a whole, such that, in 2020, the annual increase ratio will amount to 4.0%.

By 2020, the IMF projects domestic economic growth to rise to 1.3%, driven by a moderate recovery in domestic demand stemming from the dissipation of uncertainty. Precariously, this rate approximates that of population growth, resulting in zero growth in average purchasing power or GDP per capita.

It is to be hoped that we will witness efforts to increase coverage, to deploy new generation networks, which should ideally be accompanied by the deepening demand and consumption of services. I have only said that ideally they should do it, we will see their implementation effectiveness.

Additionally, the generation of conditions of effective competition is required to advance in generating incentives for capitalization and the deployment of infrastructure.

From the first months of 2020, the regulator must seek the realization of competition based on asymmetric regulation of preponderance, as the best known way to break the structural rigidity of market concentration enjoyed by the preponderant, with the consequent harmful effects on consumers and their competitors.

Text written by Ernesto Piedras of The Competitive Intelligence Unit, CIU.