Latin America. During the third quarter of 2022 (Q3-2022), the telecommunications sector in the Ibero-American region (IbAm) generated revenues of $31,695 million dollars, 4.0% more in the annual comparison, according to statistics compiled by The Competitive Intelligence Unit (The CIU) for the Ibero-American Telecommunications Organization (OTI).

The mobile market contributes in greater proportion with 56.2% of the total ($17,801 million dollars), while 27.5% ($8,719 million dollars) corresponds to the provision of fixed telephony and broadband services, the remaining 16.3% ($5,175 million dollars) is attributable to Restricted or pay television.

Mobile telecommunications recorded the best performance by increasing their revenues by 6.0% driven by the intensification in the adoption and use of these ubiquitous services by the inhabitants in the countries of the region, while the fixed and Restricted TV segments reached a moderate growth of 5.4% and 3.7%, respectively.

This positive evolution is attributable to the boost in the contracting and consumption of telecommunications among individuals, households and companies in the countries of the region, derived from an improvement in the relative prices of telecommunications services in an inflationary situation of the rest of the goods, together with an improvement in the supply of fixed services. and their packaging that have become attractive and accessible to millions of homes.

The countries with the largest number of inhabitants, Brazil and Mexico are the main markets, together accounting for 46.6% of the aggregate revenues of the IbAm region. These are followed by Spain, Argentina and Colombia with a proportion of 12.8%, 8.0% and 6.4% respectively. Finally, it highlights a weighting of 4.5% of the Chilean market and 4.3% of the Peruvian market, the first despite registering smaller population size, stands out as one of the countries with the greatest expansion of the telecommunications sector.

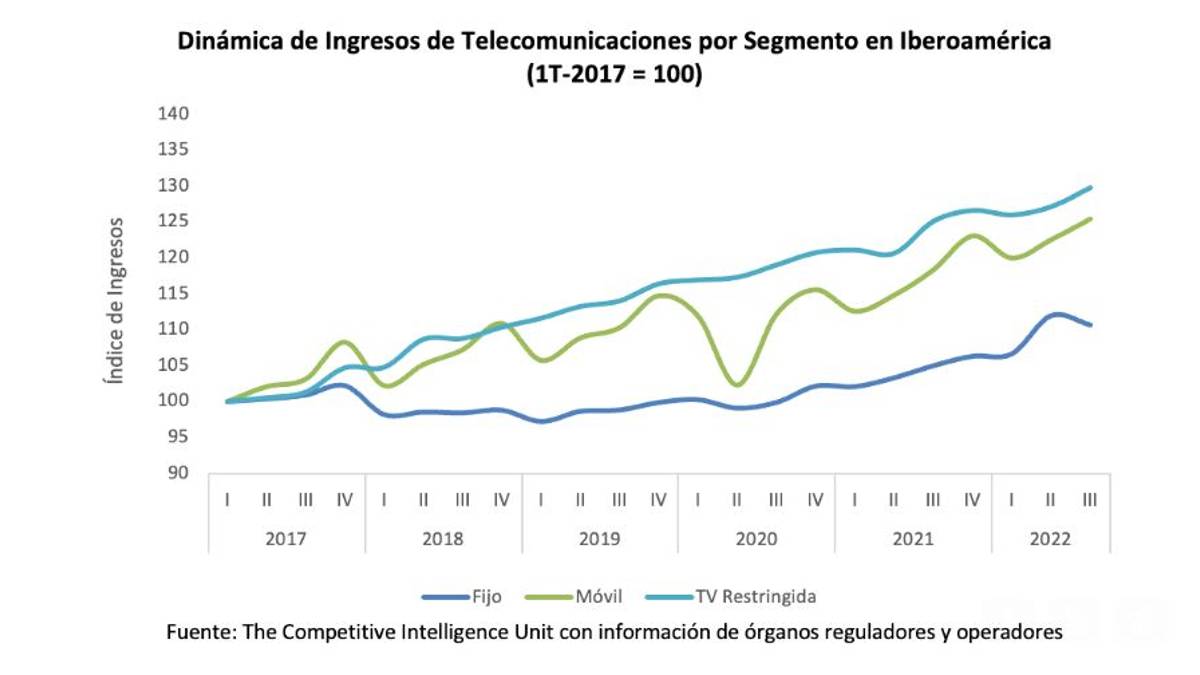

The IbAm region continues to chart an upward trajectory in revenues for all three segments of the sector. In the fixed segment, there is a slight slowdown in its growth compared to previous quarters. On the other hand, the rest of the member markets maintain an upward trajectory in their income dynamics.

Although the mobile segment has levels of widespread adoption of services in most countries in the region, it is on an accelerated growth path in terms of revenue. While restricted TV maintains its relevance and growth, even when competing head-on with audiovisual alternatives over the internet, content piracy and the disconnection of the service in the face of the economic crisis faced by some countries.

Since 2017, the dynamics of revenue by segment have been upward but differentiated between the different segments. Mobile telecommunications trace a volatility in their growth trajectory, a circumstance that was accentuated at the beginning of the COVID-19 pandemic. However, since the first half of 2021, it resumed its upward path, registering an average annual rate of 6.3% in Q3-2022.

The volatility is attributable to the economic shocks that impact this market eminently under the modality of low consumption prepayment, with a dependence on the availability of resources, such that at the end of the year a rebound is usually observed, while at the beginning of the year a fall associated with the "January slope".

On the other hand, fixed telephony, broadband and restricted television services show moderate behaviour, but trace an upward trajectory with contained variations. Since the first quarter of 2021 (Q1-2021), the fixed segment averages 4.8% annual rate, while restricted TV 4.2%. In other words, these services average growth 1.5 and 2.1 percentage points below the mobile segment, despite the volatility of the latter. The less variable behavior is attributable to the conclusion of fixed-term contracts and mostly constant consumption patterns, together with the growing adoption of these services in households in the region.

With the recovery of economic dynamism, OTI anticipates that the favorable growth prospects of the sector will continue, based on greater demand and consumption of connectivity services. On the one hand, the needs of ubiquitous connection, the laying of state-of-the-art networks and the intensification in the use of the capabilities of the deployed infrastructure, will drive the mobile segment. On the other hand, the demand for low-cost high-speed connections and the growing preference for service bundling will set the growth pattern for fixed and restricted TV services.

However, other economic and social factors that may adversely affect sectoral performance are identified. For example, inflationary pressures, the relative price of currencies, bottlenecks in international trade and high interest rates in the international context can impact both the supply of telecommunications services, due to higher costs, and the consumption of such services, due to the behavior of people's disposable income.

For example, the constitutional crisis in Chile, rampant inflation in Argentina, the political crisis in Colombia or Peru, youth unemployment in Spain, insecurity in Ecuador or Mexico, are phenomena that can undermine the performance of their economies and telecommunications sectors. Likewise, the short-term challenges of each market in the region may contain the adoption of services, the growth of the sector and the deployment of state-of-the-art networks.

Finally, OTI warns that, although the telecommunications sector will continue to be one of the engines of growth in the countries, the risks that threaten the economies of the region cannot be underestimated, so it is up to all actors, regulatory and administrative authorities, as well as the operators themselves, to adopt measures or strategies to prevent a crisis that negatively impacts the sectoral dynamism. Hence, the convenience of defining objectives, strategies and public and regulatory policies that encourage economic competition, innovation, investment, connectivity and deployment of infrastructures in the Ibero-American region.