Latin America. The telecommunications sector has shown transcendental changes in recent years: the entry of new companies into the market, strategic alliances between competitors, establishment of specific rules for the dominant operator in the market, among others. All this has brought important changes, the reconfiguration of the sector and new business opportunities.

Latin America. The telecommunications sector has shown transcendental changes in recent years: the entry of new companies into the market, strategic alliances between competitors, establishment of specific rules for the dominant operator in the market, among others. All this has brought important changes, the reconfiguration of the sector and new business opportunities.

Likewise, the world economy has been drastically transformed, the engines of growth that existed until a few years ago have lost their dynamism. The political environment also sees important changes that could transform global trade. However, the good performance of domestic consumption, controlled inflation rates and a healthy financial system predict that international impacts will not greatly impact the performance of the Telecommunications sector for 2017.

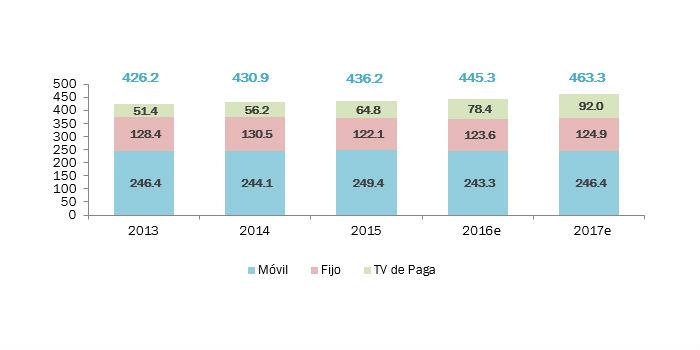

According to recent estimates by The Competitive Intelligence Unit, at the end of 2016, the telecommunications sector as a whole generated $445,291 million pesos, reaching an annual growth of 2.1% during the year, below the forecast coefficient of 3.4%1 that the economy as a whole will present. However, this forecast is more optimistic for 2017, where growth of 4.0% is expected, as a result of the greater dynamism of the national productive apparatus, equivalent to a growth rate of 4.1%, as well as the consolidation of the effects of the price reduction on the adoption and consumption of services.

In its composition by segments, trends vary significantly. We can observe, contrary to 2015, a favorable performance for the fixed telecommunications segment, derived from the stabilization of fixed telephony prices and a significant growth in broadband revenues, all despite a decrease of 2.1% of fixed telephony subscribers. In this way, this market is expected to register an annual growth in revenues equivalent to 1.2% in 2016, to reach a value of $123,586 million pesos and a share of 27.7% within the total generated by telecommunications. It is expected that by 2017 this sector will continue this slight upward trend (1.1% annual growth) guided by fixed connectivity services.

When analyzing the mobile services market, by the end of 2016 it was estimated that the market would show a significant decline in terms of income because the continuous drop in prices has not yet been able to be compensated by the increase in subscribers and consumption of services. The year is forecast to close with a decline of 2.4%, reaching a weighting of 54.6% in the total income of the sector. It is expected that during 2017 and 2018 the price decrease will stabilize in the face of the new market ecosystem. It is estimated that the higher growth in economic activity, the increase in the customer base, together with the deepening in the consumption of mobile services, especially mobile broadband, triggers a growth in the segment of 1.3% in 2017.

Meanwhile, the cable telecommunications and satellite television segment is the one that will present the highest growth rate, increasing 21.0% in the revenue category with respect to the previous year, reaching $78,416 million during 2016, corresponding to an increase in the share within total revenues of one percentage point from 17.6%. In this way, the segment is constituted as the driver of growth in the sector. This dynamism derives both from the significant growth of satellite television in Mexico, as well as from the incessant increase in the user base of packaged services, as a result of the important economies presented by its adoption in terms of prices. It is forecast that for 2017 this segment will grow at a rate of 17.3%, attributable to the continuous growth of the customer base as a result of the offer of better tariff and service conditions in this market.

After this quantitative count of the sector, a favorable forecast is expected for 2017 around the benefits of the new competitive ecosystem, the injection of greater infrastructure resources, the sharing of infrastructure, as well as the increase in the basket of services offered. It is expected that from this year the new upward ramp of growth of the sector will be shown, as a result of the greater coverage of services, the deepening of the consumption of services, aimed at achieving its universal adoption among Mexicans.

Text written by Carlos Hernández, from The Competitive Intelligence Unit

Chart: The Competitive Intelligence Unit estimates with operator information