Latin America. The possible acquisition of Warner Bros. (WB) by Netflix or Paramount is a significant milestone for the global audiovisual value chain. The Competitive Intelligence Unit analyzed the impact of this business.

Beyond the drama and corporate negotiation, it is an operation with several direct implications on levels of concentration, effective rivalry and conditions of access to content, particularly in the subscription video-on-demand (SVOD) market.

As has been pointed out since the announcement of the purchase agreement by Netflix, this operation triggers antitrust alerts due to the magnitude of the assets involved and the strategic role that WB holds in the entertainment value chain: production, intellectual property, distribution and exhibition.

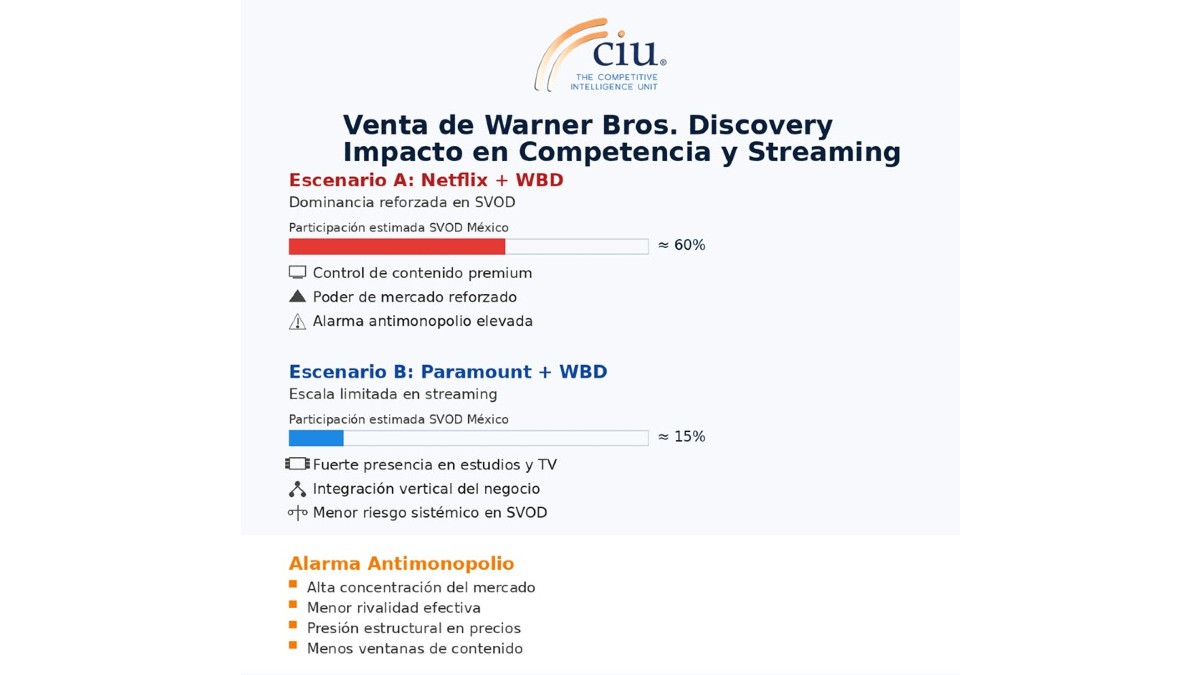

A-Netflix–Warner Bros. Scenario: Enhanced Dominance Risk

Under the scenario in which Netflix completes the acquisition of Warner Bros., the main economic effect would be the consolidation of an already dominant leadership position in the streaming market.

The merger with HBO Max, Warner Bros. Pictures and high-value global franchises would significantly strengthen Netflix's ability to set prices, access conditions and market standards.

From a quantitative perspective, the combined entity could reach a share of more than 60% in the SVOD market in Mexico, while globally it would concentrate around 40–45% of subscriptions.

This level of concentration does not necessarily imply the immediate displacement of competitors, but it does imply a significant reduction in the effective competitive pressure, as well as in the ability to match their supply conditions.

In turn, this scenario is the one that sets off antitrust alarms with the greatest brilliance, since it would combine leadership in digital distribution, control of consumer data and ownership of some of the most relevant content assets in the industry.

In Latin American countries, characterized by accelerated streaming growth but with high price sensitivity, the effects of increased concentration and a reduction in the number of players can affect price and package competition.

The central risk lies not only in prices, but in the ability to condition access to key content, limit licensing schemes and raise barriers to competitors.

B-Paramount–Warner Bros. Scenario: Potential Structural Counterweight

The alternative of an acquisition by Paramount responds to a different market logic.

In this case, the integration would seek to reconfigure competition between large conglomerates, integrating production, linear television, cable and streaming to build an actor with greater scale against Netflix and Disney.

Under this scenario, Paramount and WB's combined market share could stand at 15% in the streaming market, with a more diversified distribution between digital platforms and traditional assets.

While it would increase the level of concentration, its competitive impact differs: it does not reinforce the existing leader, but rather strengthens a competing player.

From the point of view of economic competition, this scenario poses risks more associated with integration, particularly in audiovisual production and distribution.

However, it could also contribute to preserving a more balanced market structure, provided that there are regulatory safeguards in place to prevent exclusivity or anti-competitive bundling.

Antitrust Alarms and Potential Regulatory Remedies

The possible sale of Warner Bros. triggers antitrust alarms globally and in Mexico by registering high levels of concentration and marked economies of scale in the SVOD market.

In this sense, greater consolidation can translate into less rivalry, reduced alternatives for audiences and greater pressure on the audiovisual value chain.

For competition authorities, the challenge will be to assess dynamic effects, beyond static market shares. This involves analyzing how the operation would affect market contestability, access to essential inputs, and trading conditions in the value chain.

The possible acquisition of Warner Bros., either by Netflix or Paramount, marks a turning point in the evolution of the global audiovisual market. The first scenario deepens the risks of dominance and concentration, while the second reconfigures the competitive balance without eliminating them completely.

From a competition policy perspective, the challenge is not only to approve or block the operation, but also to ensure that the market remains contestable, with incentives for innovation, plurality of content and a diverse and affordable offer for audiences.

In that sense, the antitrust alarm is not rhetoric, but a sign of the need for rigorous evaluations and, where appropriate, proportionate regulatory remedies.

Analysis by Radamés Camargo of The Competitive Intelligence Unit, The CIU.