![]() Mexico. A notorious feature of telecommunications services is the technological convergence that results in service packaging, economies of scale, ease of billing and payment for users, and multiplatform use of various infrastructures.

Mexico. A notorious feature of telecommunications services is the technological convergence that results in service packaging, economies of scale, ease of billing and payment for users, and multiplatform use of various infrastructures.

That is clearly the case with pay-TV services over cable networks, which enable triple-play (internet, video and fixed services) and even quadruple-play (mobile services, additionally), all on the same infrastructure and equipment.

To a large extent, this is why the pay-TV segment in Mexico registers a marked dynamism in terms of income generation, subscriptions, deepening of services and investments, among other elements. All this has resulted in improvements in the quality and coverage of the service, coupled with a diversification in the services offered by migrating to a provision of packaging, with significant savings in prices for households.

Growth and Penetration of Services

According to the accounting reported by the IFT, the number of pay-TV subscribers reached 19.6 million in the second quarter of 2017, equivalent to a growth of 39.7% in the last four years.

In other words, it represents a contracting or penetration of the service in 67 out of every 100 households, a reason that is among the highest in Latin America, as a result of Mexico's advantage in terms of more competitive prices in a regional perspective.

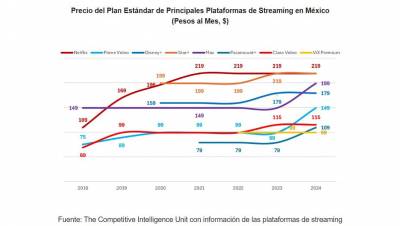

For several years, the British consultancy Ovum has identified that in Mexico the average monthly cost of basic pay-TV packages is the lowest level in the entire region ($22.2 PPP).

Dynamics of Pay-TV Investments

It is precisely this competitive impulse that has triggered the incentives for competitors to allocate greater resources in infrastructure networks to increase their coverage and quality, and in turn, enable the offer of convergent and value-added services.

Thus, between 2013 and 2016, investment in infrastructure by pay-TV operators increased 149.0%, with an annual average of 36.7%, to reach an amount of $28,038.6 million pesos in 2016, a figure that represents a third of the exercise of resources allocated to the telecommunications sector as a whole during that year.

The Conditions for Competition

This, in turn, derives from the reduced barriers to entry present in the market, for example, as there is a diversity of audiovisual content distribution platforms that are competitive with each other and as there is unrestricted access to content relevant to Mexican audiences by competitors in Pay-TV, with the regulatory implementation of must-Carry/Must-Offer.

This has led, for example, to the relatively recent incursion of the operator into the market, Star TV, which results in an addition of competition and expands the range of alternatives for consumers. Since entering the Mexican market, Star TV has sought to position itself with differentiated offers in prices, packages and pay-TV coverage and has focused its business strategy in locations where the service is scarcely provided. Currently, it reaches a market footprint in 24 states, 8 times its coverage commitment established in its concession title.

Indeed, these market conditions and dynamics are indicative of the competitive environment that characterizes the pay-TV industry in Mexico, with opportunities to attract revenue and attract subscribers for players that have triggered contestability, the exercise of capital resources in infrastructure, the diversification of the offer and the incursion of new players in the market.

Text written by Ernesto Piedras of The Competitive Intelligence Unit.

Leave your comment