Mexico. An industry that registers a high dynamism and diversification in its consumption alternatives is that of content, applications and digital services that have radically transformed other adjacent industries, for example that of transport, accommodation, home deliveries, audiovisual consumption, among others. There we find participants both of local origin, as well as those from abroad.

Mexico. An industry that registers a high dynamism and diversification in its consumption alternatives is that of content, applications and digital services that have radically transformed other adjacent industries, for example that of transport, accommodation, home deliveries, audiovisual consumption, among others. There we find participants both of local origin, as well as those from abroad.

It is desirable to generate equitable conditions for the operation of both sets of players, in a scenario in which the competitive level has resulted in significant improvements in price and quality of goods and services for final consumers in our country.

However, with the pressing need for fiscal resources on the part of the State, it is intended to take advantage of the delay in the legal and tax framework in order to be subject to VAT on digital services of final consumption for individuals or households in Mexico.

Lessons from the International Arena

Although at the international level, various international organizations such as the OECD, ECLAC, OAS, ITU and CET. LA propose the updating and modification of national regulatory frameworks to level the competitive terrain in the face of the irruption of foreign digital players, the different territories have not implemented the application of VAT to all digital services indiscriminately.

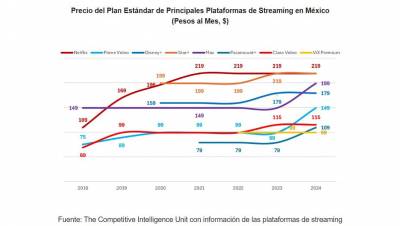

This tax leveling and even the imposition of special taxes has been especially applicable to foreign providers and platforms of audiovisual content by subscription, such as Netflix and Amazon Prime Video, due to the marked competitive imbalance that takes place against players of national origin.

In Mexico, it is intended to apply VAT to a wide variety of digital products and services, according to the Explanatory Memorandum of the Value Added Tax Law corresponding to the fiscal miscellaneous for 2020, approved in recent days in the Chamber of Deputies.

Even an initiative was recently announced that seeks the imposition of the IEPS on the commercialization of consoles and video games, without evidence or antecedent of application of special taxes, beyond those on income or added value. In fact, in European countries there are tax incentives for the continuous generation of games and technological development, such are the cases of the United Kingdom and France.

Possible Distortions to Digital Access and Consumption

Although the Explanatory Memorandum of the VAT Law states that this is not a new tax burden, it will be transferred and borne by final consumers, in their capacity as importers of products and services.

Among the basic economic principles that a tax must comply with is simplicity, equity, effectiveness and collection efficiency. It is precisely this principle that would not be sought here, since the imposition of VAT on digital services would raise a barrier to access and distort their consumption, even of those that have even proven to generate positive externalities by enhancing productivity, growth and development of individuals, households and MSMEs.

It merits that the Mexican State questions the convenience and necessity of the application of VAT to practically the entire digital economy, especially in light of its mission to achieve a full connectivity scenario in Mexico. To do this, it must level the competitive terrain with national players and at the same time, avoid generating distortions in the access and use of digital services for Mexicans.

Text written by Ernesto Piedras, from The Competitive Intelligence Unit.

Leave your comment