Mexico. The metrics of the telecommunications sector in the first quarter of the current year show a continued dynamism in terms of users and revenues, resulting from the growing contracting of services and the intensification of the use of its connectivity services, in both fixed and mobile modalities.

Mexico. The metrics of the telecommunications sector in the first quarter of the current year show a continued dynamism in terms of users and revenues, resulting from the growing contracting of services and the intensification of the use of its connectivity services, in both fixed and mobile modalities.

In the first quarter of 2019 (Q1-2019), revenues generated by all telecommunications companies grew at an annual rate of 2.6%, that is, 7.7 times higher than the economy as a whole (GDP growth of 0.2%).

Telecom Mobile

The mobile segment that generates 6 out of 10 pesos of the sectoral total illustrates to a large extent the evolution and competitive missteps of the market in general.

Consumption in terms of lines and mobile data intensity increased to result in annual growth of 3.0% during the quarter. But this growth dynamic was not homogeneous among operators, with the preponderant (Telcel) taking the most advantage of its condition.

In competitive terms, at the beginning of the asymmetric regulation process, the preponderant Telcel accounted for 73.0% of the revenues of the mobile segment. With the application of the first asymmetric regulation measures, at the time of the first review mandated to the regulatory body, IFT, that participation stood at 68.1%.

The exhaustion of its benefits and its insufficiency in application or even disarticulation (as in the case of zero interconnection), now result in losses of competitive ground to date. The figures for Q1-2019 show a preponderant that reappropriated 3.3 percentage points more of total mobile revenues, reaching a market share of 71.4%, today closer to its level at the time of the establishment of the preponderance, than to that at the best moment of the competition.

Although it has been anticipated that América Móvil may take 15 years to abandon its status as a preponderant agent, the continued trend of this competitive regression would now result in the absolute concentration of revenues in the mobile segment in 18 years. That is, a mobile monopoly. Worse and faster, if business doors are added to new fields of business, such as restricted TV.

Fixed Telecom

The fixed segment continued the packaging of double or triple play services and the creation of aggressive and competitive strategies by operators in the provision of internet, as well as an improvement in the conditions of supply to the final consumer.

However, despite the fact that fixed broadband service registers a stable growth in upstream contracting, it has been insufficient to compensate for the fall in segment revenues (-6.6% in Q1-2019) derived from the loss of added value due to the use of fixed telephone lines.

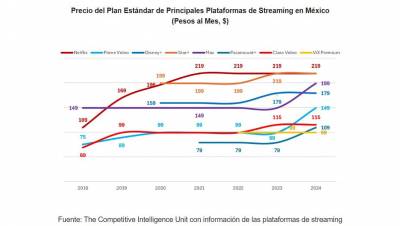

Pay-TV and Converged Services

The Pay-TV market resumed its usual double-digit growth dynamics in terms of growth (10.4%), despite registering a contraction in the satellite technology subscriber base of 8.3% per year, more than offset by the growth in cable service contracting (10.6%), attributable to the attractiveness and economies involving the subscription to double and triple play packages.

This is how the sector outlines a positive growth dynamic during 2019, higher than that of the national economy, as a result of the increase in consumption, the contracting of services, the aggressiveness of the offers of competitors, the packaging of services and the improvement in their quality.

The continuation of the Q1-2019 trend and its permanence on a positive path will depend to a large extent on the competitive balance between operators, the best conditions for the deployment of infrastructure and the effectiveness of asymmetric regulation in terms of effective competition.

Text written by Ernesto Piedras of The Competitive Intelligence Unit, CIU.

Leave your comment