Mexico. Fiscal policy (collection and allocation of public expenditure and investment) is more than just a set of accounting entries, it is an instrument for the promotion of development, stability and equity.

Mexico. Fiscal policy (collection and allocation of public expenditure and investment) is more than just a set of accounting entries, it is an instrument for the promotion of development, stability and equity.

Especially with the latter, fiscal equity, Mexico has chosen not only to eliminate the windows that allow foreign suppliers to sell services to Mexicans without informing the Mexican treasury of the taxes that correspond as would happen if the service were supplied from Mexican territory, but also by the leveling of the competitive terrain in the field of audiovisual content, between domestic companies and foreign Internet video (OTT) platforms.

In the search for such a leveling of the operational terrain, legislators recently approved the Revenue Law of the Federation corresponding to the year 2020, which incorporates modifications in tax matters applicable to digital players.

This seeks to advance in the elimination of the competitive imbalance in the audiovisual content market, with the updating of the regulatory and fiscal frameworks in national legalization. It is indeed an update, but based on successful experiences already applied in other countries and on recommendations from international organizations, which seek to standardize tax and regulatory burdens between the different ways of audiovisual consumption, leaving behind the scenario of legal vacuum and regulatory laxity that has benefited digital platforms and services.

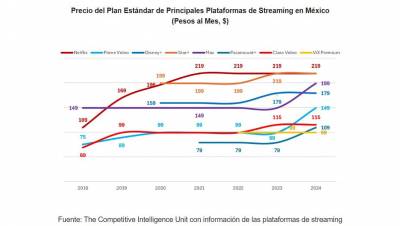

Experiences in LatAm

ECLAC has documented how countries in the region have implemented reforms to incorporate digital players into the fiscal framework. [1] Most of the initiatives (Argentina, Chile, Colombia, Costa Rica, Paraguay and Uruguay, among others) seek competitive equity based on the modification of their legal frameworks to ensure the application of full VAT in the value chain of foreign companies that offer audiovisual services over the Internet.

For example, for their collection they rely, in some cases, on the retention by financial institutions, through their credit or debit cards (Argentina, Chile, Costa Rica and Paraguay), while in others, the platforms are required to register in a registry of taxpayers in the territory of operation, to facilitate the full payment of their tax contribution (Colombia and Uruguay).

ECLAC emphasizes the importance of other countries in the region also making efforts to make progress in this area, following internationally recommended practices.

Its recommendation is precisely to modify national legislation so that foreign companies are subject to VAT, accompanied by the design of mechanisms to ensure effective collection.

Next Steps in Mexico

In Mexico, by parliamentary initiative and the SHCP, foreign digital platforms and services for the generation and distribution of audiovisual content, such as Netflix, Amazon Prime Video and HBO GO, will be subject to VAT.

This tax modification is inserted in line with the regional experiences described and does not imply the creation of excise duties or new levies. It simply consists of the homologation of tax burdens between local and international, traditional and digital players.

New? Not so much, it is simply a tax update according to the form of commercial operation of today and, even more, of the future. Our country takes the opportunity to advance in updating the tax framework that had a lag of 7 years, to begin to align with international proposals, practices and recommendations.

Thus, it is glimpsed to begin to leave behind the current scenario that has resulted in tax evasion, inequality and competitive imbalance in favor of foreign digital platforms. In stark contrast to Mexican companies that invest in the generation of content, from the incorporation and training of national talent, while contributing to the fiscal ladder and, with it, to the economic development of the country.

It was time for equity and fiscal and regulatory updating for competitive equity, in the face of the irruption of digital platforms.

Text written by Ernesto Piedras of The Competitive Intelligence Unit.

Leave your comment