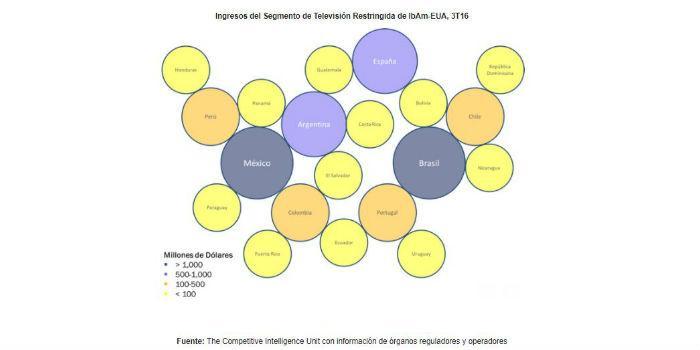

Latin America. The restricted television segment in the integral region of Ibero-America and the United States of America (IbAm-USA) recorded revenues of $33,961 million dollars during the third quarter of 2016 (3Q16), this is an annual growth of 6.6% in constant dollars compared to the same period of the previous year. Particularly, in Latin America, revenues of $6,726 million dollars were generated, equivalent to an annual growth of 23.6%.

Latin America. The restricted television segment in the integral region of Ibero-America and the United States of America (IbAm-USA) recorded revenues of $33,961 million dollars during the third quarter of 2016 (3Q16), this is an annual growth of 6.6% in constant dollars compared to the same period of the previous year. Particularly, in Latin America, revenues of $6,726 million dollars were generated, equivalent to an annual growth of 23.6%.

According to the latest report on the subject of the Ibero-American Telecommunications Organization, OTI, all the countries of the region register an increase in the segment's revenues compared to the same period of the previous year. In this area, Argentina and Honduras stand out, where revenues increased by more than 30% per year. Particularly, in Mexico there is a growth of 17.7%, in Colombia 11.5%, Brazil 9.2%, Chile 7.7% and the United States 3.1%. The upward trend in the hiring of restricted television service is one of the main causes of the growth in revenues.

Subregional case: Central America

The average growth in Central American revenues, for the Pay-TV segment, has been maintained in recent years at ratios between 5% and 10%, with an average annual growth of 9.9% for the region as a whole, when comparing the third quarter of 2016 with the same period of the previous year. The positive trend and constant adoption of the service, although still limited, in the countries of this subregion generate a scenario of prospective expansion of this segment.

The existence of more mature markets, in terms of infrastructure development, such as Costa Rica, Honduras and Panama creates important opportunities for expansion in contracting and, therefore, for restricted television revenues and convergent services in general. The increasing digitalization of networks makes it possible to offer Triple Play packaged services (pay TV, voice and data). According to international market experience, the provision of converged services in a market is followed by significant growth in adoption and revenue of services, a result that is already recorded in some of these markets.

On the other hand, it is expected that the availability of satellite Pay-TV at affordable prices will continue to encourage the consumption of the service in areas of difficult coverage of physical networks. This is mainly in those countries that still register significant connectivity gaps through physical digital networks.

It is important to note that the development potential of this subregion is conditional on the existence of solutions to the security, competition and investment challenges that still characterize it. Solving these conditions will provide certainty and competitiveness to the markets, encouraging the growth of local and regional operators, but with improvements in quality and prices for end users.

Both the introduction of basic packages aimed at the incorporation of the low-income population, and the packaging of services make the service offer more attractive. These elements have been essential to increase the user base of the service and, consequently, have driven revenue generation. Additionally, the increase in the expenditure of restricted TV subscribers, motivated by the offer of new value-added services and convergent services, has generated an increase in the average revenue per subscriber (ARPU) which results in growth more than proportional to those of the user base.

Leave your comment