Increases in tariffs and additional charges in streaming by subscription reduce the well-being of users.

Radamés Camargo*

The subscription streaming platform market has seen changes in its pricing strategy, subscription plan offer, business model and contracting conditions for access to content, in the search to achieve better results in terms of profits, acquisition and user retention capacity.

This has led to the fact that since the end of 2022, some of the main players in this market have introduced advertising in their subscription plans at a lower price, imposed locks on the sharing of accounts/passwords and recently, opted to charge additional fees to avoid the interruption of commercials in the playback of content.

This change in the contracting conditions has generated discontent among users, a circumstance that is added to the recent price increases of the platforms, which previously benefited from low rates, zero advertising in the content and zero 'extra' charges for access to services.

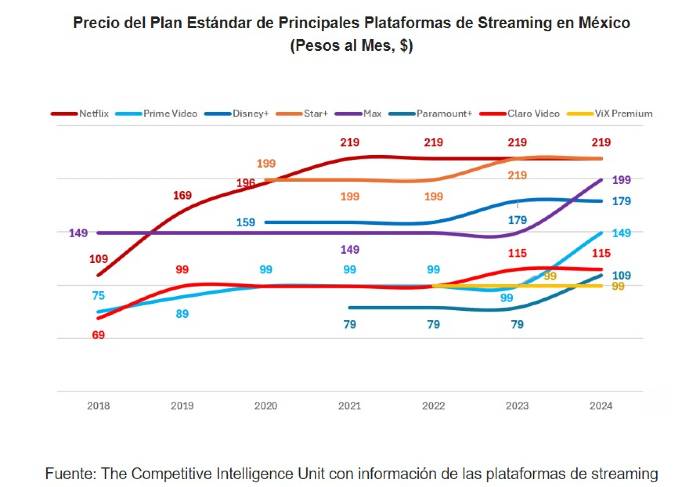

Rising Streaming Rates

The main and incumbent player in the market, Netflix, has made constant increases in the price of its different subscription plans, even during the pandemic, despite the economic crisis and confinement in homes. Although the last rate increase took place in 2021, at the end of 2023, it eliminated the 'basic' plan that allowed access to the platform without advertising for only $40 pesos difference compared to the standard plan with ads. Currently, to avoid advertising interruption, users have to pay three times that amount ($120 pesos per month). Additionally, the platform requires the payment of $69 pesos per month for each extra user (up to two), to share the account outside the contracting address.

Another of the players that has applied constant price increases to its subscription has been Amazon Prime Video, from 2018 to date, it has raised its prices on four occasions, the last one being in recent weeks with the virtual tariff increase that implies the extra charge of $50 pesos (+50.5%) to watch content without commercial guidelines, the highest among its competitors. Precisely, users perceive this additional charge as a price increase, as they require an additional outlay to be able to enjoy the service under the previous contracting conditions.

Despite receiving income from advertisers for the inclusion of commercials, the player has decided to apply an additional fee, causing categorical discontent among users and has even resulted in a class action lawsuit in the United States.

All of this erects significant economic barriers for users who found advantages through pricing when contracting subscription video platforms.

Other platforms such as Disney+, Star+, Max and Paramount+ have recently increased their prices by up to 33.6% in their standard subscription plans and in the case of the first two they will make available an integrated offer with advertising at a lower price in the following months, while the latter already have these plans.

This with the purpose of strengthening its financial positioning and loyalty with its users, in the face of growing competition and strong investments in original content that require a diversification of revenue streams for streaming platforms.

This with the purpose of strengthening its financial positioning and loyalty with its users, in the face of growing competition and strong investments in original content that require a diversification of revenue streams for streaming platforms.

In contrast to previous players, ViX Premium continues with its introductory price, with marked savings (savings of +50%) in the contracting of its annual plan. This is in recognition of the purchasing power and well-being of consumers, by having affordable alternatives, free access to ad-supported content and a vast catalog of Spanish-language titles.

Prospective Market Effects

The implementation of strategies of price increases in the subscription and additional charges to avoid advertisements and/or sharing the account with people outside the contracting address, has not only generated discontent among users, but has even translated, since the second half of last year, into a reconfiguration in the preference and number of contracted platforms.

This has resulted in a boost in the participation of players other than the main one that offer alternatives for access to audiovisual content by subscription at lower prices, and has simultaneously reduced the contracting of three or more platforms, by erecting greater budgetary barriers for users.

While streaming players are looking to have healthy finances that make their direct-to-consumer content delivery business model sustainable in the short term, they should not fail to consider the advantages that drove preference and hiring in this market. That is, the offer of affordable alternatives, free of advertisements and lower economic barriers to their contracting.

Undoubtedly, this scenario should be a cause for concern for platforms in the medium and long term, in the search to attract and continue to 'loyalty' users, who benefited from marked savings in the contracting of subscription streaming alternatives and who today have more and more options for accessing content for free.

*Radamés Carmargo is Analysis manager at The Competitive Intelligence Unit, The CIU.